The VIX futures are holding a significant spread to the VIX. Let’s explore what this could mean to the VXX, which rolls 1st into 2nd month futures during the VIX futures cycle. First, here are the futures:

| Symbol | Contract | Month | Time | Last | Change | Open | High | Low |

|---|---|---|---|---|---|---|---|---|

| VX N3-CF | S&P 500 VOLATILITY | July2013 | 17:28:49 | 18.85 | -0.60 | 19.00 | 19.35 | 18.75 |

| VX Q3-CF | S&P 500 VOLATILITY | August2013 | 17:28:49 | 19.60 | -0.35 | 19.60 | 19.90 | 19.43 |

| VX U3-CF | S&P 500 VOLATILITY | September2013 | 17:28:49 | 20.40 | -0.15 | 20.25 | 20.50 | 20.10 |

Now the recent divergence between the VIX and VXX:

The spread of VIX spot to the front month (July) is 9.5% and to 2nd month in which the VXX rolls every day is 14%. At this point the weights are roughly 75% July and 25% August. Just to give you a little perspective, August VIX in 2013 fell into the 13’s at times, and was 13.45 at expiration. All spikes in vol shorted last summer were very profitable trades.

Due to the size of the spread, I went back and looked at times when these conditions occurred:

1. Spread of VIX front month to spot of 8%+

2. VIX spiking to over 18 just before this occurred

This eliminated all of the high spreads to spot VIX over the last year when the VIX was under 14. It is understandable that the VIX futures would sit at 14 when the VIX spot is 12 with significant time to expiration. Any movement lower in index prices would send the VIX significantly higher.

These conditions do not happen very often. In fact, the most recent occurrences were, amazingly enough, late June, late July, and late August of last year. The VXX did not fare well after these conditions existed:

June 2012- Late June to July expiration- VXX fell 26 Priligy%

July 2012- Late July to Aug expiration- VXX fell 22%

Aug 2012- Late Aug to Sep expiration- VXX fell 25%

Most of the losses in the VXX came early in the expiration month. A simple way to think of these scenarios is that the VIX futures are expecting more volatility, and the VXX has big shoes to fill with the futures trading so high above index options volatility and with a sizeable roll. The market must sell-off significantly for the VXX to actually rise, as there is such a huge volatility buffer built into its price. In fact, it would be normal to see the S&P fall on some days and have the VXX fall with it.

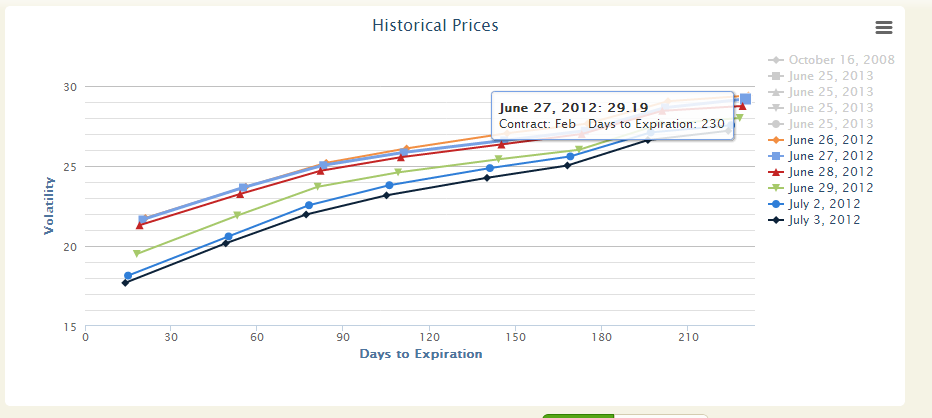

Here is an example of how the futures behaved during the June 2012 period, courtesy of vixcentral.com:

I will do more research to see how often the futures actually portend of more volatility on the horizon, but a quick study seems to suggest that the futures are a head fake.

One other important point here, is that the holiday, with shortened trading Wednesday, no trading Thursday, and low volume Friday tend to suck out a ton of premium and implied volatility. In anticipation of these events, Thursday-Wednesday could see a significant drop in implied volatility. On Monday the 8th, the VIX futures will have only 9 trading days to expiration.

The VXX has major headwinds right now. The market could easily resume selling-off and spiking vol, but if the sell-offs are moderate as opposed to 40 point down days, the VXX will have a tough time going higher. Expectations for vol are high in the VIX futures term structure.

I am long VXX July $18 and $19 puts, and sold a vertical VXX call spread expiring next week at $22-24 for .52.